Last updated: July 2026

A quick word before we start. I am writing this as a guide for my community, not as the word of law. A lot of people here are genuinely lost when it comes to banking in Pakistan, and good information on this stuff is scarce.

So I want to share what I have picked up over the years in a safe and honest way, and hopefully close some of that gap. But everything here is my own experience, not financial or tax advice.

This world changes fast. If you are unsure about anything, please talk to your accountant, or come join the community and talk it through with your peers. I want to help, and I want to do it the right way.

– Saqib

We have a banking debate in my community almost every month. Someone opens the wrong account. Someone gets hit with a charge they did not expect. Someone asks whether the freelancer account is worth it, and off we go again. I have answered the same questions so many times that the regulars now call it my bhajan.

So I am writing it down once.

Everything I know about banking in Pakistan, in one place.

Fair warning before we start. There is no good bank in Pakistan. There is no clean recommendation waiting at the end of this where I tell you “open this one and you are sorted”.

We have bad options and worse options. The whole game is picking the least-bad one for what you actually need, and knowing which traps are waiting for you on the way in.

This is not only for freelancers. A freelancer has specific needs and gets their own section, but most of what follows is just banking literacy for anyone in Pakistan trying to hold and move money without getting quietly robbed by fees, bad apps, and processes designed in 1995.

TL;DR: There is no good bank in Pakistan, only the least-bad one for your need. Open a regular account, never a freelancer (or any special account). Keep it to 2 accounts, maybe 3: one legacy branch bank (Meezan or UBL), one digital (Mashreq for me), optionally a wallet for small stuff. If foreign income is landing, pick a bank that auto-generates your PRC (your proof of foreign income). Ignore cashback, read the account type instead, and accept that your branch locality and staff in there matters more than the logo on the card.

What’s covered, in order:

- Banking in Pakistan Is a Field of Traps

- Wallets Are Not Banks (and When That’s Fine)

- The Freelancer Account Is a Trap

- How Many Bank Accounts You Actually Need

- Card Fees, Virtual Cards, and the Cashback Myth

- Getting Paid From Abroad: Foreign Income Banking in Pakistan

- Filer Status and Banking in Pakistan

- Banking in Pakistan as a Registered Business

- Islamic vs Conventional Banking in Pakistan

- My Personal Bank Verdicts (Read the Disclaimer First)

- A Few Rules Before You Open Anything

- The Bottom Line on Banking in Pakistan

- Banking in Pakistan FAQs

Banking in Pakistan Is a Field of Traps

Start with the right mindset, because it saves you the most money. Banking in Pakistan is not a product you buy, it is a minefield you cross. Almost every “feature” a bank or a wallet waves at you has a catch behind it, and the catch is usually a fee, a lock-in, or an account type that quietly earns you less.

The first trap is not even at the bank. It is borrowing. Credit cards, EMI plans, “0% installment” offers, buy-now-pay-later, all of it is built to feel like convenience while it slowly makes you complacent. EMI is an endless cycle of ruin dressed up as convenience. My rule here is boring and it has served me well. If you cannot afford to buy something, you should not buy it. I have never taken a loan in my life despite being able to, and that discipline is load-bearing to everything else I have built. Banks make a large chunk of their money lending out your deposits and charging interest on the way back. Try not to be on the paying side of that.

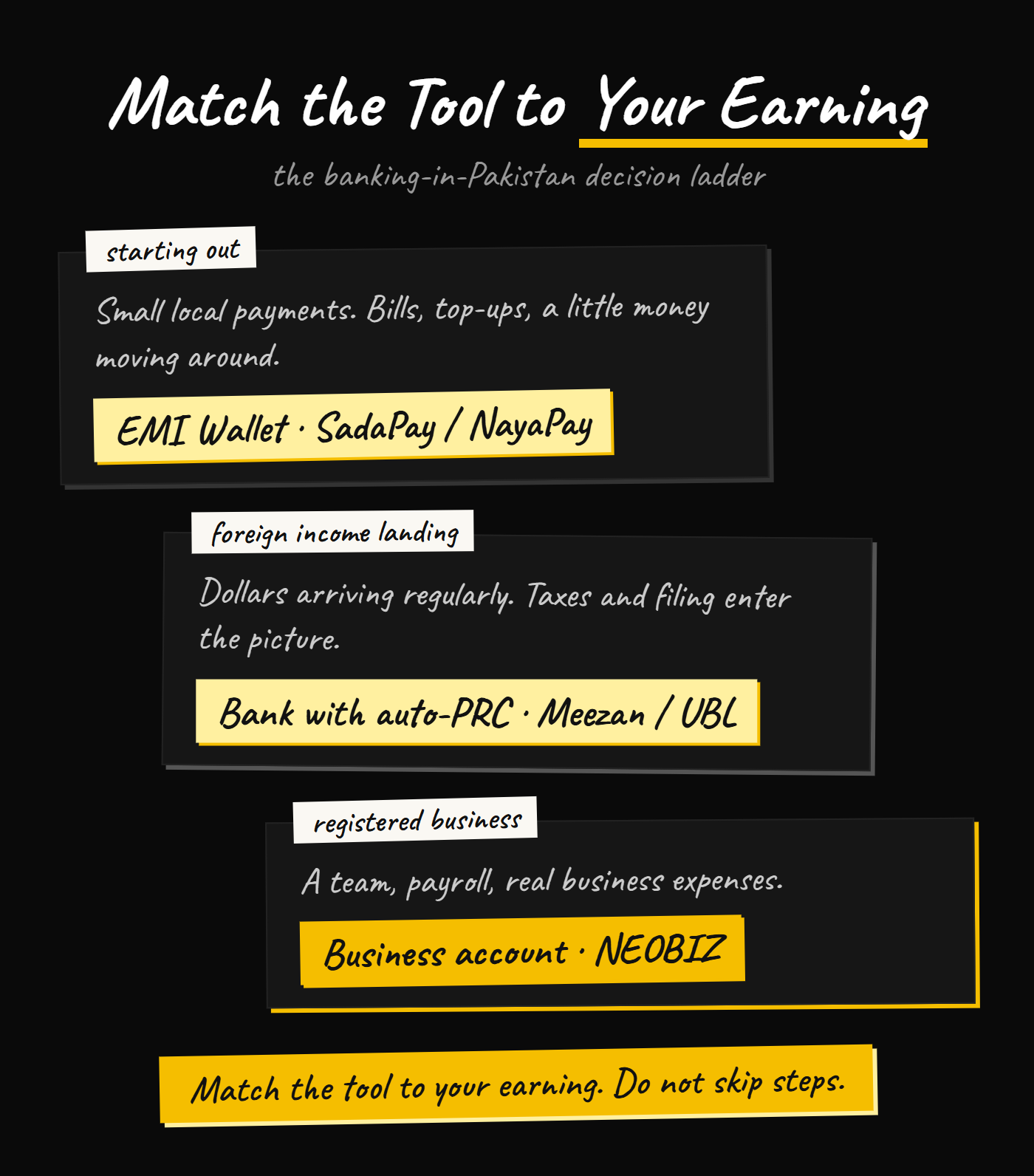

The second piece: banking is not for kids. I say that half as a joke and half seriously. If you are 19, earning a bit here and there, and you are worried about a Rs.2,500 card fee, you are not ready for a bank account and you do not need one yet. That is what wallets are for. Real banking starts to matter when you are moving real money, receiving foreign income, or running a business. Until then, keep it simple.

Everything below is really just a tour of the traps, and how to step around each one.

Wallets Are Not Banks (and When That’s Fine)

SadaPay, NayaPay, Easypaisa, JazzCash. These are EMI wallets, not banks (some are banks now, but you get the point). They are regulated by the State Bank, they give you an IBAN so people can transfer into them, and they are cheaper and far less painful to open than a bank account. For a lot of people starting out with banking in Pakistan, that is genuinely all you need.

If you are early, doing small local transactions, paying for mobile packages and bills, and the annual charge on a bank debit card feels like a real cost, then stick to a wallet. There is no shame in it. It is the correct move. Open a proper bank account when you actually have a reason to. One habit worth building at this stage: track where your money goes. The Personal Expense Tracker guide covers how I do it.

A couple of practical notes, if a wallet is going to be your daily driver:

| Wallet | Foreign conversion | Free ATM withdrawals | Leans toward |

|---|---|---|---|

| SadaPay | Flat fee (~1.5% last I checked) | Limited | Simple daily use |

| NayaPay | Lets Visa set the rate | Historically a few free on Alfalah and UBL machines | Transfers, bill payments |

Small differences, but they add up if you live inside one of these.

Now the important carve-out, because this is where people get it wrong. If you are a freelancer receiving foreign income, do not assume a wallet is enough. What you need is clean documentation for filing, specifically the PRC (Proceeds Realization Certificate) that proves your foreign money came in through a legitimate channel with the right purpose code (9186 for IT and freelance export earnings).

Banks like Meezan and UBL auto-generate these, which is the whole point of keeping one. Wallets are murkier, and I want to be straight that I have not fully confirmed this, so treat it as a caveat, not a ruling. From what I can find, NayaPay can now get you a 9186 PRC, but only on money that arrives through a specific route (its Elevate Pay salary-transfer flow), only after you email a request for it, and it is issued through their partner banks anyway. I have not seen a clean, documented path on SadaPay at all. So a wallet PRC is a hassle at best, not a given. Worse, foreign money that lands in a wallet through the wrong channel can get flagged as unexplained income at tax time, which is a fight you do not want.

So the “just use a wallet” advice is for general beginners and small local use. The moment dollars are landing regularly, a proper bank that auto-issues your PRC is the cleaner, safer move, and you are in bank territory. More on that below.

One more thing worth saying out loud. SadaPay and NayaPay were genuinely great a couple of years ago. They have been sliding lately, more delays, more random declines on normal transactions. Use them for what they are good at, do not build your financial life on top of one.

The Freelancer Account Is a Trap

Freelancer accounts are a scam. Open a regular account.

The backstory explains it. Around 2023, the State Bank effectively ran a quota. Every bank was told to open as many freelancer accounts as possible, so they went around pushing them on anyone with even $1 of foreign income. The whole point was optics, they could inflate export-board numbers and claim the freelance economy was booming. I knew back then there was a catch, and that eventually they would regulate and restrict these accounts. That is exactly what happened.

The trap was the easy entry. A freelancer account skipped the proof-of-income requirement a normal account asks for, so people opted in because it was less hassle. Now, opening one is a different story. In some cases they physically visit and photograph your remote setup to verify you actually are a freelancer. The gimmick that was easy to get into is now the harder, more restricted option. (This part is my own experience and what I have watched happen to people around me, not a documented regulation, so treat it as such).

The takeaway is simple. Skip the freelancer account. Open a normal account. If what you want is the digital, no-proof-of-income convenience that made freelancer accounts attractive in the first place, the clean way to get that today is a fully digital bank, which brings us to how many accounts you actually need.

How Many Bank Accounts You Actually Need

2 minimum, 3 maximum. More than that and you are just creating admin for yourself.

The rule I keep repeating:

| Account | My pick | Why you keep it |

|---|---|---|

| One legacy branch bank | A big legacy bank with auto-PRC (my picks are in the verdicts below) | Branch infrastructure when you need it: a cheque book, a pay order, a physical place to walk into when something breaks. Your fallback, kabhi zarurat parh sakti hai. |

| One digital bank | The one you actually like using (mine is in the verdicts below) | Your day-to-day, the one you actually live in, because it does not send you to a branch for every small thing. |

| Optionally, one wallet | SadaPay or NayaPay | Small local stuff (mobile top-ups, small payments), only if you want the convenience. |

The third step of that ladder is for registered businesses only. A business account joins the setup on top of the personal accounts, not instead of them. That case gets its own section below.

That is it. I spent years experimenting across most of the banks on the market, and I have spent the last couple of years closing accounts, not opening them. Standard Chartered, Alfalah, MCB, Allied, HBL, all shut. If you are collecting accounts, you are collecting problems. Pick 2, maybe 3, close the rest.

Card Fees, Virtual Cards, and the Cashback Myth

All bank debit and credit cards are paid. Expect roughly Rs.2,500 a year plus federal excise duty, and the exact number depends entirely on the card tier. A silver-tier card at one of the big banks might be around Rs.3,000, closer to Rs.7,000 once you add tax and SMS charges. A Visa costs differently from a Mastercard, and a Platinum tier costs more again. There is no flat “card fee”, so read the schedule before you pick.

Wallets have warped everyone’s sense of what banking in Pakistan should cost. Because SadaPay and Easypaisa gave you a “free” card, a Rs.2,500 bank charge feels outrageous. It is not, it is just what a real bank card costs.

Now cashback, because this is the biggest myth in Pakistani banking. Cashback is bait. Unless you are spending 3 to 4 lac a month on the specific applicable channels, the amount you get back is noise. The old cashback credit cards were mostly useless, which is why people who understood the game moved to points-based cards, where you can actually use the points however you want. Do not pick an account or a card for the cashback.

The current version of this trap is one digital bank’s own cashback push. So many people opened their savings account (which earns) that they are now promoting a current account (which returns roughly half) dressed up with cashback offers. Same rule applies. The account type is what matters, the cashback is the distraction. Do not fall for it.

Virtual cards deserve their own note, because people misunderstand what they are for. A virtual card is good for one job: online and digital subscriptions. Use it for that. It is easy to manage, and if the number leaks you just kill it and generate a new one. Most services give them out free right now (physical cards cost money to produce), though I fully expect traditional banks to start charging for virtual cards too once enough people are onboarded.

The misunderstanding that burns people: disabling a virtual card does not cancel your subscription. The merchant already has it on file and can still charge you. Killing the card only stops a leaked number from being used for new charges. To actually stop a recurring charge, you cancel the subscription itself. There is no shortcut, and every month someone gets confused, gets charged, or gets an account blocked because they thought deleting the card would do it.

(One line on tap-to-pay: Google Wallet on Android now carries a lot of virtual cards, so you can tap to pay without a physical card, but the infrastructure is still flaky even in a main city like Islamabad, so outside the big cities, keep a physical card, and if your bank’s card is too pricey, get one off a wallet.)

Last card note: some banks’ debit cards often will not work on international sites, which is exactly why people move funds to a wallet’s virtual card to pay online. The bank-by-bank detail is in my verdicts below.

Getting Paid From Abroad: Foreign Income Banking in Pakistan

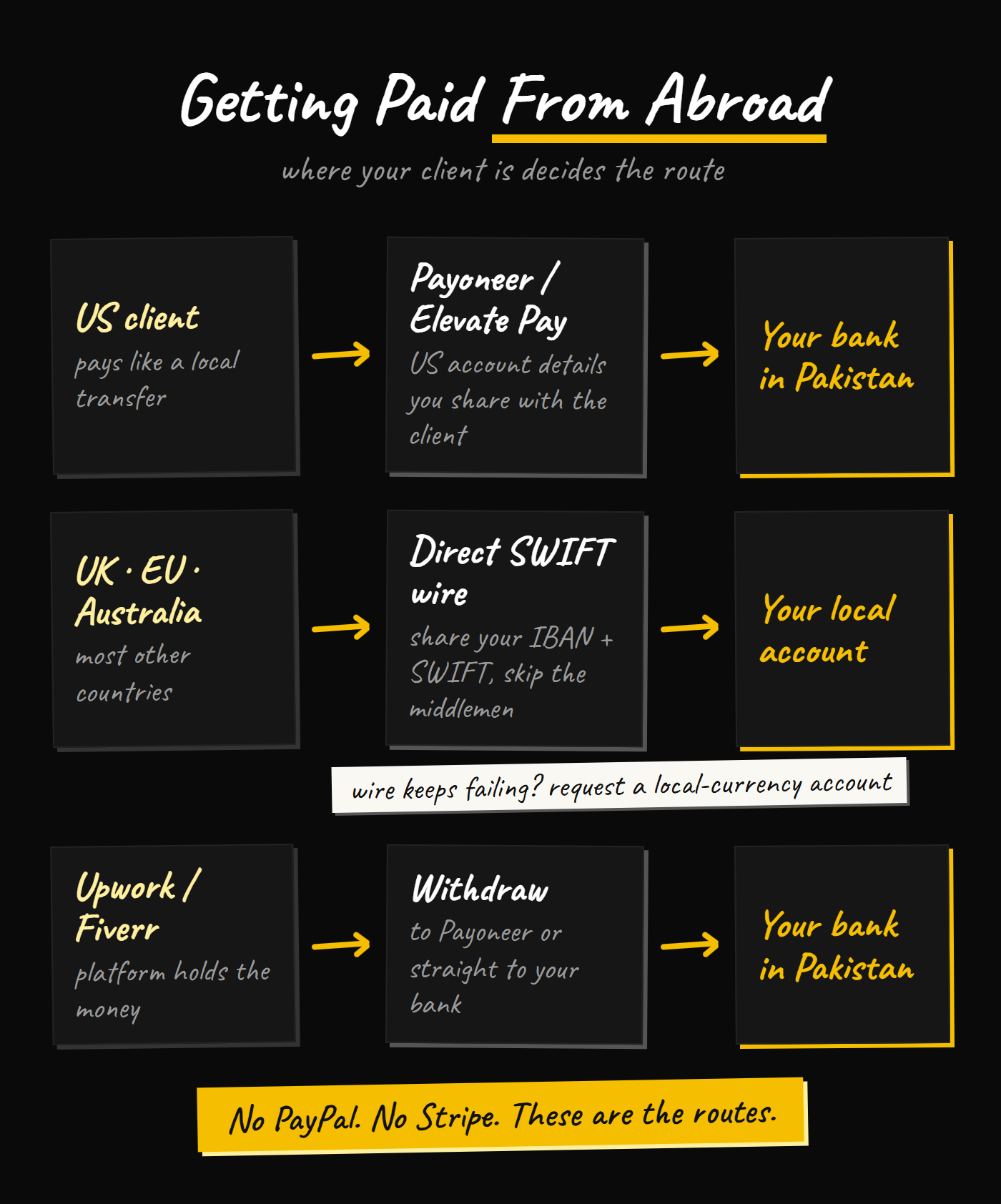

This is where banking in Pakistan actually hurts. Freelancers and remote workers feel the pain the most, and the options are genuinely limited. It depends heavily on where your client is.

If you are getting paid from the US, you have a few options, and all of them give you a US-based bank account whose details you share with the client so they can do a simple bank transfer:

| Service | My take |

|---|---|

| Payoneer | The default. Works, integrates with the platforms, what most people use. Also charges a lot and has been enshittifying for years, so it is the workhorse, not the hero. |

| Elevate Pay | Another solid US-client option worth looking at. |

| Remitly | Testing it right now, cannot recommend it yet, but it is on the list. |

| Xoom | Exists too. I have not used it, so I cannot vouch for it. |

If your client is in the UK, Australia, or most other places, skip the middlemen entirely. Share your local bank details, your IBAN and SWIFT, and have them wire the money directly into your account. One local quirk to know: some countries (Australia is a notable one) struggle to send money into a USD account, but they handle a local-currency account fine. So if a transfer keeps failing, request a local-currency account and route it there.

And if you are on a freelancing platform like Upwork or Fiverr, they hold the money for you and let you withdraw to Payoneer or straight to your bank. The platforms themselves are a separate, longer conversation, and I have written about where those platforms are actually heading if you want that context.

While we are here, the question everyone eventually asks: why is there no PayPal or Stripe in Pakistan? The blunt answer is corruption and regulation. A large share of the economy runs on undocumented money, and a service like PayPal or Stripe cannot operate cleanly in that environment, because using them would force everything into the white. So we are stuck with the workarounds above. That is the system working as designed, not an accident.

Filer Status and Banking in Pakistan

I will keep this short because I have written a full Taxation 101 for Pakistani freelancers guide, and I would rather not duplicate it. But a few things are specifically banking decisions, not just tax ones.

Be a filer. Full stop. Not becoming a filer is like kicking a can down the street, eventually you have to pick it up, and it is more expensive by then. Non-filers pay significantly higher withholding on almost everything, from bank profit to card transactions.

The banking-specific move: let your bank deduct the tax on your foreign income (broadly around 1% of gross freelance income under current rules). It costs you the same either way, and having the bank do it gives you a clean record that proves your income source. That paper trail is worth more than the small hassle it saves you.

And this is where the PRC from the wallets section comes back: you need it to file properly, and you do not want to be begging a branch to generate one manually every year. Pick a bank that auto-generates PRCs on incoming foreign remittance. Meezan does this well, and UBL has started doing it too. That single feature is a big reason I keep the accounts I keep.

Rates and thresholds change every budget, so verify the current numbers with FBR or an accountant before you act. Do not take a figure in an article (including this one) as gospel on tax.

Banking in Pakistan as a Registered Business

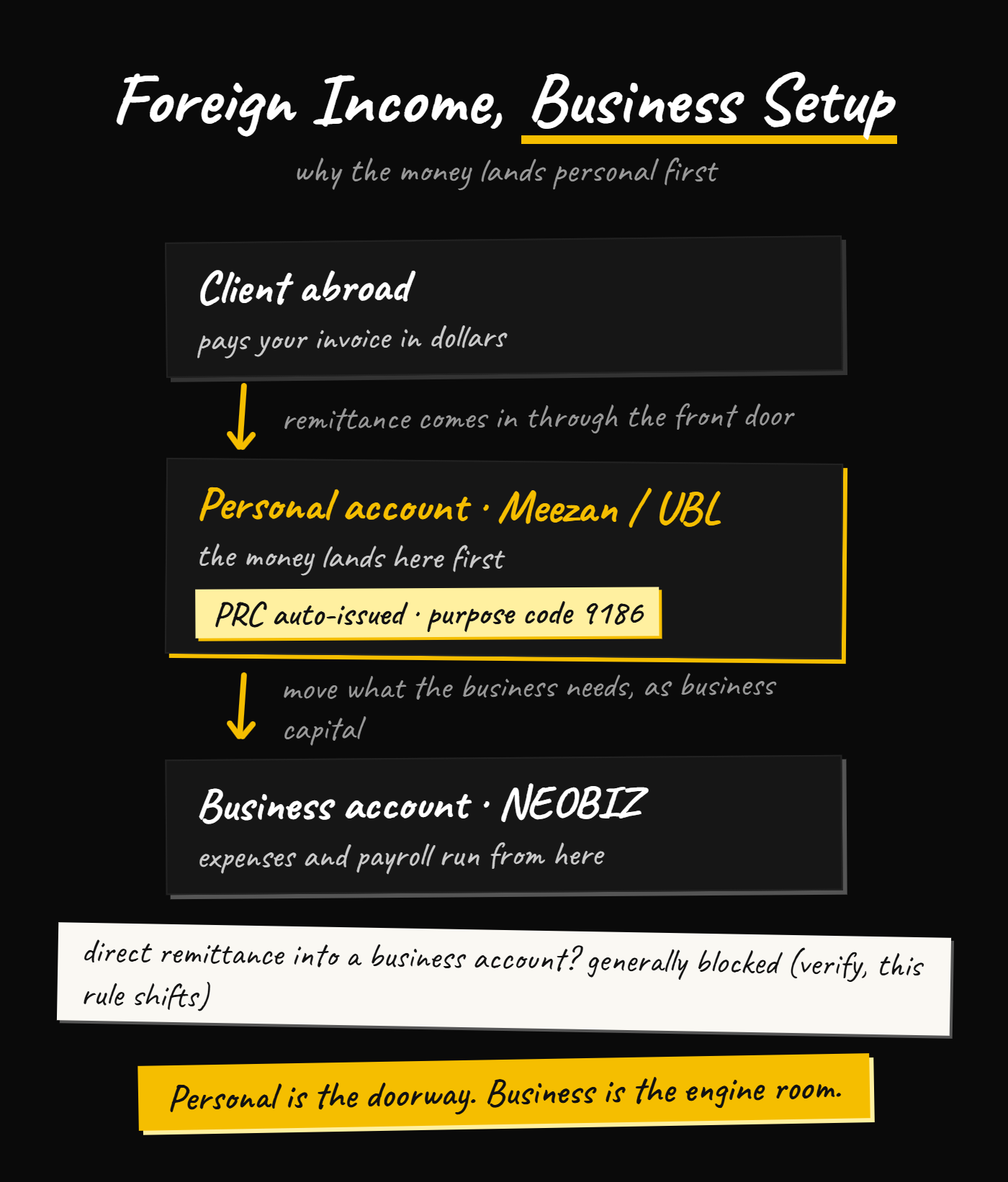

Everything above assumes you are an individual. If you have a registered business, the rules change.

A registered business needs a business account. There is no clean way around it, and trying to run business money through a personal account creates problems. What you want is a business account you can open fully digitally, no branch visits, that hooks into your NTN cleanly. Exactly one bank does this well right now, and that story is in my verdicts below.

Now the mechanic that trips people up. As I understand it (and this is one to verify, because it is exactly the kind of rule that shifts), you generally cannot receive foreign remittance directly into a business account. So the money has to land in a personal account first. That is another reason you keep a dedicated personal account with good PRC support, Meezan or UBL, to bring the foreign income in.

From there it depends on your setup:

If you are a one-person business, you can honestly just run it yourself out of the personal account and not overthink it.

If you are running a team, hiring, and paying salaries, move the income into the business account and run your business expenses and payroll from there. What I suggest is treating a chunk of that money as business capital, park it in the business account, and run expenses off it, until the day remittances can hit business accounts directly and easily. That day may come. It is not here yet.

Islamic vs Conventional Banking in Pakistan

This one confuses a lot of people, and it is worth understanding rather than just picking “Islamic” because it sounds safer.

The usual question: how can an Islamic savings account pay a return without that being interest?

A common take, and I hear it in the community too, is that the whole thing is the same product with a halal sticker on it. At the marketing level, where the labels are sometimes loosely regulated, the skepticism is fair. Underneath though, the two models differ where it counts: who carries the risk, how the spreads work, and what happens to you on a missed payment.

The short version. Conventional banking loans out money and charges interest that must be paid back regardless of what happens. Guaranteed return to the lender, which is what makes it riba. Islamic banking is profit-sharing (Mudaraba). Your money is used to buy and invest into asset-tied units, the bank takes a service fee, and the profit generated is shared. Because not every asset earns, the profit is not guaranteed and a loss is possible. So it is a slightly higher risk model that needs larger amounts moving around to work.

A friend in the community put the principle cleanly: rent is payment for use with risk, interest is payment for time with no risk. Islam allows the first and forbids the second. The framing an imam gave: you can rent out a house because the house stays and comes back to you, but you cannot rent money, because money gets spent and is gone.

A concrete example that makes the difference click. Say you miss paying off a credit card. A conventional card charges you daily interest (usually 30% to 40% a year), so on a Rs.100 balance you owe about Rs.140 a year later. An Islamic card cannot charge interest, so instead it fines you a flat amount for non-payment, often around Rs.5,000 a month regardless of how much you owe. So miss that same Rs.100, and a year of flat Rs.5,000 fines later you owe about Rs.60,100. Different model, different risk, and it can bite you in ways you did not expect.

Side by side:

| Conventional | Islamic (Mudaraba) | |

|---|---|---|

| How it earns | Lends out money, charges interest | Invests in asset-tied units, shares the profit |

| Your return | Guaranteed (which is what makes it riba) | Not guaranteed, a loss is possible |

| Risk to you | Lower | Slightly higher |

| If you miss a card payment | Daily interest (~30% to 40% a year): Rs.100 becomes ~Rs.140 | Flat fine (~Rs.5,000 a month): Rs.100 becomes ~Rs.60,100 |

| Where your money goes | Any legal business | Shariah-compliant businesses only |

One more difference, and by my read the one that should matter most: an Islamic bank is only allowed to put your money into Shariah-compliant businesses.

Your deposits cannot end up funding alcohol, gambling, or interest-based lending on the other side. For a lot of people that is the entire point, and it is a real, structural difference, whatever you make of the labels.

The usual caveat applies though: that is the theory. And the theory is genuinely good, shared risk and transparent installments, good enough that in the UK, a lot of fixed-deposit customers are not even Muslim. They pick it on merit.

Practice is another matter in a system as corrupt as ours, and there is a serious argument, from a former finance minister, that Islamic banking here tracks the conventional system far more closely than the definitions suggest.

However, this is a banking guide, not a borrowing or investing one, so for a regular account holder the fundamentals above are what you are choosing between. Just know the practice debate exists.

One caveat worth conceding though. Both systems have matured so much that from the outside, for a normal account holder, the day-to-day difference is small.

And it is worth knowing that all banks in Pakistan are mandated to convert to Islamic banking by the end of this decade, so this distinction is heading toward moot anyway.

Pick based on your own conviction, not because one sounds automatically better.

My Personal Bank Verdicts (Read the Disclaimer First)

Everything in this section is my personal experience across 14+ years of banking in Pakistan, using nearly every bank in the country, HBL, UBL, Alfalah, Meezan, Allied, Faysal, Al Habib, MCB, Standard Chartered, and now Mashreq. Your mileage will vary, and I mean that literally, because of the single biggest confound in Pakistani banking.

Branch and staff quality is the real variable. Protocols are State-Bank-mandated and identical across banks, but training is not. Some branches are running processes 2 years out of date, and the same bank can be a completely different experience from one branch to the next. If you live near a good, active, well-run branch, you are lucky, and half your problems disappear. If you do not, good luck.

To show you how bad it gets: I once opened an HBL account, and the woman at the counter did not know how to register me for the mobile app. She took my phone, typed my name and a random password into the app, and tried to log in, to an account that did not exist yet. When I pointed out you cannot log into an account before it is created, she rolled her eyes and asked if I knew better than her. This was a branch in a well-off area, supposedly trained. That is the baseline you are working with, so weigh my verdicts accordingly.

With that said, my read, in the bad-vs-worse spirit. The quick version to scan first, with the detail underneath:

| Bank | Best for | Watch out for |

|---|---|---|

| UBL | Best all-rounder for most people: best app, good card, now auto-generates PRCs | Branch support can be genuinely bad |

| Meezan | Branch strength, purely Islamic, best PRC generation, 250k one-shot ATM withdrawal | Weak app UI, debit card struggles online |

| HBL | Best credit card, historically | Not much else pulls me to it |

| Mashreq | Best digital experience: fully digital, no branch visits, Askari-backed, 3-click zakat exemption, savings-first | New here, so support has not scaled; some Android bugs |

| Alfalah | Nothing I would steer you toward | Cost me 20k to 30k on a filer-status tax error, 4 visits for a zakat exemption, buggy app (my worst run) |

UBL is the best all-rounder for most people right now. Best app UI and UX among the older banks, better card usage, and it now auto-generates PRCs. The catch is branch support, which can be genuinely bad. But for the average person, this is where I would point you.

Meezan is your pick if you want branch strength or a purely Islamic bank. It also has the best PRC generation and one real standout: its ATM lets you withdraw 250k in a single shot, which is great in an emergency. The downsides are a weak app UI and a debit card that struggles online.

HBL has historically had the best credit card. That is mostly what it is worth to me.

Mashreq is the best digital experience I have had, and it is what I actually use day to day. It is genuinely fully digital, no branch visits, backed by Askari for branch services (so it is a real bank, unlike the wallets), it files your zakat exemption in about 3 clicks, and its first product is savings, which earns. The caveats: it is new here, so customer service has not fully scaled yet, and some Android devices have a login or performance bug. But it is the only bank that has made me feel good about banking in a long time.

The business side is the same story. NEOBIZ, their business product, is the only Islamic business account I know of that opens fully digitally. The standout moment was onboarding: I put in my NTN and it fetched my registered business automatically and hooked everything up. Every other bank buries you in documentation for this. I plugged in the number, scanned a few documents, did verification over the phone, and I was done.

Alfalah was my worst experience, and this is firmly a personal verdict. 4 visits just to get a zakat exemption. An app that lists my login name as “customer” with no way to change it. A transaction limit I could not raise past 10 lac without a branch visit. Crashes and buggy transaction exports. And the one that actually cost me money, they cut tax on my remittance despite me being registered and self-filing, and double-charged CGT because my filer status was not updated, which lost me somewhere around 20k to 30k. I closed it.

A quick technical aside, because it explains a lot of app complaints. Bank apps run worse on low-market-share devices. If you are on a Motorola or even certain Samsung models, some of the pain is Android optimization, not just the bank. Android optimization is a nightmare that nobody has solved, Google cannot even keep its own YouTube app smooth on Android.

For the record, after all that closing, my actual lineup: a personal Mashreq account, a Mashreq NEOBIZ business account, and a Meezan account for savings and PRC. Notice that my personal recommendation for most people (UBL) is not even in my own lineup. That is deliberate. What is best for you depends on your need, not on what I use.

A Few Rules Before You Open Anything

A couple of things that will save you real money and real headaches:

- Use your branch-bank card at ATMs, not your digital-bank card. Digital banks do not own their own ATMs. If a machine captures your card (and machines here still do this, or eat cash, or debit you without dispensing), a captured card is far easier to recover when it belongs to the same bank as the ATM. Use a foreign card in a random machine and good luck getting it back easily. People in my community have had 5k debited without cash coming out, and cards nearly eaten. Withdraw cash on your old-school branch-bank card, and keep the digital bank for everything digital.

- Keep your filer status updated with your bank. My Alfalah CGT mess happened precisely because the bank had stale filer information. Tell your bank when your status changes, and check that it is reflected, or you will get taxed as if you are a non-filer.

The Bottom Line on Banking in Pakistan

There is no good bank in Pakistan. There is only the least-bad one for your specific need, and the traps you learn to step around.

If you remember nothing else about banking in Pakistan:

- Open a regular account, not a freelancer one.

- Learn the difference between an EMI wallet and an actual bank, and use whichever fits your earning.

- Keep it to 2 accounts, maybe 3, one legacy and one digital.

- Pick a bank that auto-generates your PRC, so filing does not become a branch pilgrimage.

- Ignore cashback and read the account type instead.

- Accept that your branch matters more than the logo on the card.

One last thing, because banking is never really about banking. Money is fuel, not the destination. The reason to get this right is not to become someone who obsesses over accounts and cashback points, it is so the boring stuff runs in the background while you get on with the actual work. Sort your banking once, define what “enough” looks like for you, and stop letting a broken system quietly tax your attention along with your money.

And since all of this changes constantly, treat this guide as a map, not a manual.

One last reminder, since you made it all the way here. Everything above is just me sharing my own experience to help a community that too often has to figure this stuff out alone. It is not gospel, and it is not financial or tax advice. The rules and the banks change all the time, so please verify anything that matters, loop in your accountant when it counts, and if you are still unsure, come talk it through with your peers in the community. That is exactly what it is there for.

– Saqib

With or without my help – I wish you the best.

Come Build With Us

400+ members showing up, shipping work, and helping each other get better.

Or keep going: the Workshops and Templates & Tools →

Banking in Pakistan FAQs

The questions that come up in the community over and over. Short, direct answers here, with the detail in the sections above.

Which bank is best for freelancers in Pakistan?

There is no single best, only the least-bad fit for your situation. For most people I point to UBL: the best app among the older banks, decent cards, and it now auto-generates PRCs on foreign remittance. If you want branch strength or a purely Islamic bank, go Meezan, which also has the best PRC generation I have used. The setup that actually works is a pair, one legacy branch bank for PRCs and physical infrastructure, one digital bank for day-to-day use. My full verdicts, including the banks I closed, are in the section above.

Can I receive foreign payments in SadaPay or NayaPay?

Money can land there, that is not the problem. Documentation is. For tax filing you need a PRC with the right purpose code, and wallets are murky on that front. From what I can find, NayaPay only issues a 9186 PRC on money arriving through its Elevate Pay salary-transfer route, on email request, through partner banks. I have not seen a documented path on SadaPay at all. Foreign money arriving through the wrong channel can also get flagged as unexplained income at tax time. Occasional small amounts, you will survive. Regular dollars, use a bank that auto-issues PRCs.

What is a PRC and why does it matter?

A Proceeds Realization Certificate is your bank’s proof that foreign money landed in your account through a legitimate channel, tagged with a purpose code (9186 covers IT and freelance export earnings). You need it to file properly and to claim the export-income tax treatment. The practical move is to pick a bank that auto-generates PRCs on incoming remittance, Meezan or UBL, so filing season does not turn into a branch pilgrimage.

Do I need a freelancer account to receive foreign income?

No. A regular account receives foreign remittance just fine. Freelancer accounts were pushed hard around 2023 because banks had quotas to fill, and the easy entry that made them attractive is gone, they are now the harder, more restricted option, in some cases with physical verification of your work setup. Skip them. If what you want is digital convenience without branch visits, open an account with a fully digital bank instead.

Why is there no PayPal or Stripe in Pakistan?

They have never launched here, so the routes are the workarounds: Payoneer or Elevate Pay for US clients, direct SWIFT wires from most other countries, and platform withdrawals for Upwork and Fiverr work. As for why, too much of the economy runs on undocumented money, and services like PayPal and Stripe cannot operate in a market they cannot document. Do not hold your breath for a launch date.

How much tax do freelancers pay on foreign income in Pakistan?

Broadly around 1% of gross freelance income under current rules, and the clean move is letting your bank deduct it, which gives you a paper trail proving your income source. But rates and thresholds shift with every budget, so verify the current numbers with FBR or an accountant before acting. The full breakdown is in my Taxation 101 for Pakistani freelancers guide.

Is Mashreq a real bank in Pakistan?

Yes. Mashreq is a licensed bank, not an EMI wallet, and it is backed by Askari for branch services where a physical process is unavoidable. The difference from a legacy bank is that it is digital-first: fully digital account opening, no branch visits, and things like zakat exemption filed in about 3 clicks. The caveats are that it is new to the market, customer support has not fully scaled, and some Android devices hit login or performance bugs.

What is the difference between an EMI wallet and a bank?

EMI wallets (SadaPay, NayaPay, Easypaisa, JazzCash) are State Bank regulated and give you an IBAN, but they are not banks. They are cheap and easy to open, which makes them the right tool for small local use: bills, top-ups, small transfers. A bank gives you the full infrastructure: cheque books, pay orders, PRCs on foreign remittance, higher limits, and cards that cost real money. The rule for banking in Pakistan is simple, wallet while you are small and local, bank once foreign income and taxes enter the picture.

Can a business account receive foreign remittance in Pakistan?

Generally no, as I understand it, and this is one to verify because it is exactly the kind of rule that shifts. Foreign money has to land in a personal account first, which is why you keep a dedicated personal account with good PRC support even after opening a business account. From there, move what the business needs into the business account and run expenses and payroll off it.

Are Islamic bank accounts in Pakistan actually interest-free?

By structure, yes. Islamic banking runs on profit-sharing (Mudaraba): your money is invested into asset-tied units and the profit is shared, so the return is not guaranteed and a loss is possible, which is what keeps it from being riba. What surprises people is the penalty model. An Islamic card cannot charge interest on a missed payment, so it fines a flat amount instead, which can cost far more than interest would. And note that all banks in Pakistan are mandated to convert to Islamic banking by the end of this decade, so the distinction is heading toward moot.

See, at the heart of it – I love solving problems for people using tech, it doesn’t get simpler than that.

I am known for constant experimentation and relentless execution.

Right now – my focus is to help everyday folks of Pakistan understand tech, career, and business better with everything I do.